A short note before we begin

Real estate investing has always involved forming judgment under uncertainty.

Over time, valuation frameworks emerge — shaped by experience, market cycles, and the collective memory of past decisions. As new data and analytical tools evolve, I have become increasingly curious about how these familiar approaches might also change.

This letter shares a personal perspective informed by recent academic research, industry observation, and the ongoing process of learning while building technology for the investment community.

These reflections are also shaping how we are thinking about product design at Reml — and we look forward to sharing more tangible examples in the coming months.

How value is typically assessed in real estate today

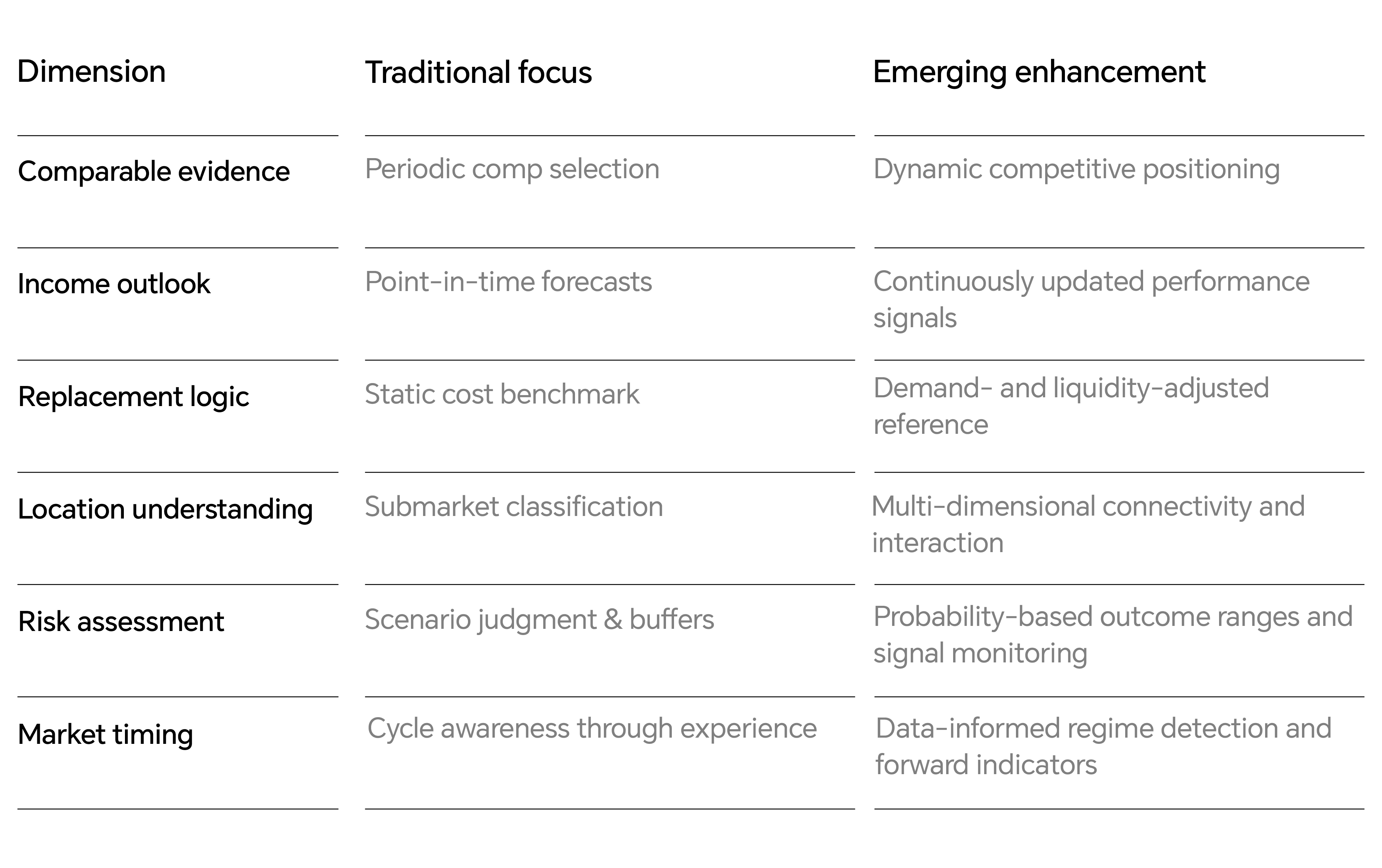

Most valuations still rely on three core foundations.

The sales comparison approach interprets recent transactions and adjusts for differences in quality, leasing profile, location, and timing. It reflects how markets actually price assets, yet reliable comparable evidence is often limited or delayed.

The income approach converts earning power into value through assumptions about rent, occupancy, and exit pricing. It anchors analysis in economic fundamentals but depends heavily on forward judgment — particularly when market conditions are changing.

The cost approach estimates replacement value adjusted for depreciation and land. It provides a useful boundary reference, although market pricing ultimately reflects demand, liquidity, and functional relevance rather than construction cost alone.

These methods remain essential.

However, they are typically applied as periodic exercises, while markets themselves evolve continuously.

Why valuation gaps continue to occur

Differences between appraisal values and realized transaction outcomes are common — and appraisal values are often higher than market pricing.

Recent research analyzing over two decades of U.S. commercial real estate data suggests that appraisal values can deviate from realized transaction prices by approximately 11% to 14% on average (Deppner et al., 2025). The same research also indicates that appraisals tend to lag underlying market movements — often trailing transaction pricing during turning points in both directions.

Timing gaps, incomplete information, and differences in perspective all contribute. Consider current in-place vacancy. One investor may interpret it as upside potential — space that can be leased and value that can be created. Another may view it as downside risk — a signal of weakening demand or possible income erosion.

Both interpretations can be rational. The real challenge lies in understanding how leasing momentum, supply conditions, and tenant behavior are evolving over time.

Traditional valuation frameworks are not designed to monitor these dynamics continuously.

Location still matters — but in higher definition

The industry’s long-standing principle — location, location, location — remains valid. What is changing is how we understand location.

Recent machine learning analysis suggests that spatial and locational factors can account for a significant portion of valuation variance — in some studies, close to 40% of the explained differences (Deppner et al., 2025).

This suggests that traditional approaches may miss important micro-spatial dynamics.

Location is no longer just an address or a submarket label. It is a dynamic network of connectivity, infrastructure, competition, and economic activity that shapes how assets perform.

In many ways, we are moving from viewing location in two dimensions to understanding it in a more multi-dimensional, high-definition perspective — similar to shifting from a static map to an immersive IMAX experience.

The role of new analytical tools

Statistical and machine-learning approaches are increasingly being used to support valuation analysis. They can organize complex information, identify nonlinear relationships, and update insights as market conditions evolve.

Models such as boosting trees have been shown to improve appraisal accuracy and reduce structural bias by capturing more complex market dynamics.

However, an important limitation remains.

For investors to trust these tools, systems cannot operate as opaque “black boxes.” Humans naturally evaluate real estate through comparison — building conviction by relating assets to one another.

The next generation of analytical systems must therefore provide clarity — not just predictions — mirroring, rather than replacing, the human intuition of comparison.

The opportunity lies in transforming outputs into reliable, explainable, and traceable decision intelligence.

This distinction is important — not all accuracy is equally useful if it cannot be understood, trusted, or acted upon.

Toward a more integrated way to evaluate assets

Bringing these ideas together suggests that valuation may gradually shift from a static conclusion to a more continuous decision process.

Rather than relying on any single methodology, investors may benefit from a more integrated framework that blends traditional discipline with continuously updated market insight.

This perspective does not replace valuation fundamentals.

It strengthens them by improving visibility, timing, and consistency — while allowing knowledge to accumulate and evolve over time.

Ultimately, better intelligence does not change what investing is — but it can change how clearly we see.

Pricing uncertainty more systematically

Uncertainty in real estate arises from imperfect data, shifting markets, human judgment, and the limits of any model.

Investors already price uncertainty through risk premiums and underwriting buffers. Yet these adjustments are often subjective and uneven, shaped by individual perspective and difficult to refine systematically over time. Much of this learning remains embedded in individual experience rather than in structured, reusable systems.

By observing signals more consistently and tracking outcomes across cycles, qualitative risks can be translated into clearer quantitative implications.

The goal is not to remove judgment, but to make it more structured, transparent, and progressively better informed.